Share

Share- Export to PDF

Listen

Listen

Malpractice insurance cost by specialty

No matter what stage of their career they are in, understanding the true cost of professional risk is a must. One of the largest — and often most confusing — expenses doctors face is medical malpractice insurance and malpractice insurance cost by specialty, which protects against claims alleging negligence or errors in patient care. Yet malpractice premiums are far from uniform. Costs can vary dramatically based on specialty, location, claims history and practice setting, leaving many physicians unsure whether they are paying a fair rate or budgeting appropriately for the future.

Whether you’re a resident choosing a specialty, an employed physician reviewing your benefits package or a practice owner planning expenses, understanding these differences can help you make smarter financial and career decisions.

How much do doctors pay for medical malpractice?

The cost of malpractice insurance for physicians in the United States spans a wide range, with premiums influenced by both individual and systemic factors. When looking at the average cost of malpractice insurance for doctors in USA, most estimates fall between $7,500 and $20,000 per year but that figure alone can be misleading without additional context.

Primary care physicians often pay toward the lower end of this range, while procedural specialists may pay several times more. Geography also plays a major role. States with higher litigation rates or less restrictive tort laws typically see higher premiums, while states with caps on noneconomic damages often experience lower costs.

Other variables that affect what doctors pay include:

- Years in practice and claims history

- Type of coverage (claims-made vs. occurrence)

- Policy limits

- Practice setting (employed vs. private practice)

- Patient volume and procedural risk

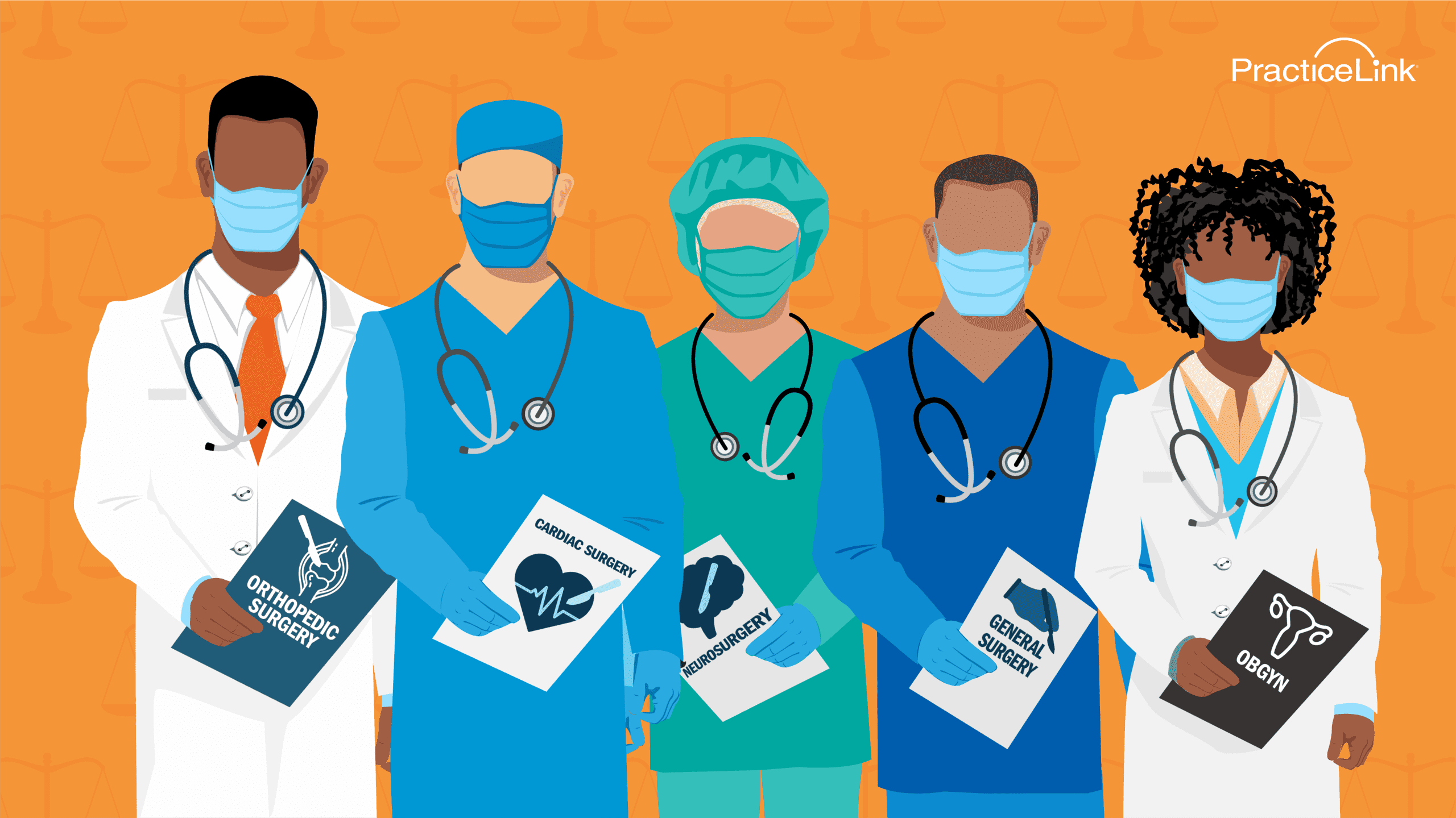

- Which doctors pay the most for malpractice insurance

When evaluating the average cost of malpractice insurance for doctors, it becomes clear very quickly that not all specialties carry the same level of legal exposure. Physicians whose work involves high-risk procedures, life-or-death decisions or complex surgical outcomes tend to face the highest premiums.

Not surprisingly, doctors who have historically paid the most for malpractice insurance include:

- Neurosurgeons

- Obstetricians and gynecologists (OB/GYNs)

- Orthopedic surgeons

- Cardiothoracic surgeons

- General surgeons

These specialties face higher claim severity, meaning when lawsuits occur, payouts are often substantial. Even if claims are relatively infrequent, the potential financial exposure drives premiums upward.

For example, OB-GYNs face significant risk related to birth injury claims, which can result in multi-million-dollar verdicts. Neurosurgeons, meanwhile, deal with extremely high-stakes outcomes involving the brain and spinal cord, where even minor complications can have devastating consequences.

What specialty has the most expensive malpractice insurance?

The question of which specialty carries the highest premiums is closely tied to malpractice insurance cost by specialty. While rankings can shift slightly year to year, neurosurgery frequently tops the list.

Neurosurgeons often pay annual premiums exceeding $150,000–$200,000, particularly in high-litigation states. OB-GYNs typically follow closely behind, with premiums commonly ranging from $60,000 to over $100,000 annually.

Other specialties with consistently high costs include:

- Orthopedic surgery

- Plastic surgery

- Cardiothoracic surgery

The combination of invasive procedures, long-term patient impact and emotional jury appeal contributes to elevated risk profiles. Insurers price policies accordingly to offset the potential for catastrophic claims.

Why is medical malpractice insurance so expensive?

Many physicians ask why premiums are so high, especially in certain fields. One key reason is that highest malpractice insurance by specialty correlates with both claim frequency and claim severity.

Several factors drive costs upward:

- High settlement and verdict amounts – Particularly in cases involving permanent disability or infant injury

- Lengthy litigation timelines – Claims can take years to resolve, increasing legal costs

- Defensive medicine pressures – Higher utilization and documentation can still fail to prevent lawsuits

- Reinsurance costs – Insurers themselves must carry coverage for catastrophic losses

Keep in mind, malpractice insurers must price policies based not only on historical claims but also on future risk. Even if a specialty should see fewer claims in a given year, the potential magnitude of a single payout keeps premiums elevated.

Is malpractice insurance a fixed cost?

Physicians often wonder whether malpractice coverage is a predictable expense. The short answer is no, because it is not fixed. Many wonder “how much is malpractice insurance per month,” and it depends on multiple variables that can change over time.

Premiums may fluctuate due to:

- Changes in specialty risk data

- New claims filed (even unresolved ones)

- Changes in coverage limits

- Moving states or switching practice types

- Market conditions within the insurance industry

For example, a surgeon paying $10,000 per month early in their career may see rates stabilize or decrease if they maintain a clean claims history, while another physician may see sudden increases after a single claim.

Breaking premiums into monthly terms can help with budgeting, but it’s important to remember insurers often view policies on an annual risk basis, not a monthly one.

Is malpractice insurance paid monthly or yearly?

Many physicians ask, “how much is malpractice insurance per year” and “must malpractice insurance be paid all at once?” While policies are typically quoted annually, it does not always have to be paid in a single lump sum.

Most insurers offer:

- Annual payment options

- Quarterly installments

- Monthly payment plans (often with small financing fees)

Physicians in private practice often prefer monthly or quarterly payments to improve cash flow, while employed physicians may have premiums covered entirely by their employer as part of a benefits package.

Regardless of payment structure, understanding the full annual cost is critical when comparing offers or evaluating compensation packages. A “covered” policy may still have lower limits or exclusions that impact real protection.

What doctors pay the highest malpractice insurance?

When comparing medical malpractice rates by specialty, procedural and surgical fields consistently rank highest. However, even within those categories, rates can vary significantly.

For instance:

- An orthopedic surgeon specializing in joint replacement may pay more than one focusing on sports medicine.

- A general surgeon performing high volumes of complex abdominal procedures may pay more than one with a narrower scope.

- A plastic surgeon performing cosmetic procedures may face different risks than one focused on reconstruction.

Volume, patient demographics and scope of practice all influence how insurers assess risk. Two physicians with the same board certification may face very different premiums based on how they practice medicine.

What medical specialty is least sued?

At the other end of the spectrum, some specialties face relatively low litigation risk. Understanding what percentage of medical malpractice cases are won helps put this into perspective.

Studies consistently show physicians win or settle favorably in most malpractice cases, with estimates suggesting doctors prevail in 60–70% of claims overall. However, claim frequency varies widely by specialty.

Specialties that are least sued often include:

- Psychiatry

- Pathology

- Radiology (diagnostic, non-interventional)

- Pediatrics (non-procedural)

- Family medicine

Lower-risk specialties tend to involve fewer invasive procedures and less immediate physical harm, which reduces both claim frequency and severity. As a result, their premiums are often among the lowest in the industry.

Understanding malpractice insurance cost by specialty is essential for making informed career, compensation and financial planning decisions. Premiums are shaped by risk exposure, specialty choice, location and practice structure — not simply by years in practice or income level.

For physicians, the key takeaway is this: malpractice insurance is not just a line-item expense, but a reflection of professional risk as well as an investment in your financial future. Knowing how your specialty compares can help you evaluate job offers, negotiate contracts and avoid being underinsured or overpaying for coverage you don’t need.

If you’re reviewing an employment offer, transitioning to private practice or reassessing your current coverage, take the time to fully understand your malpractice policy and how it aligns with your specialty-specific risk. For more guidance on navigating coverage options, costs and policy types, visit the PracticeLink Resource Center.